Responsible Boards

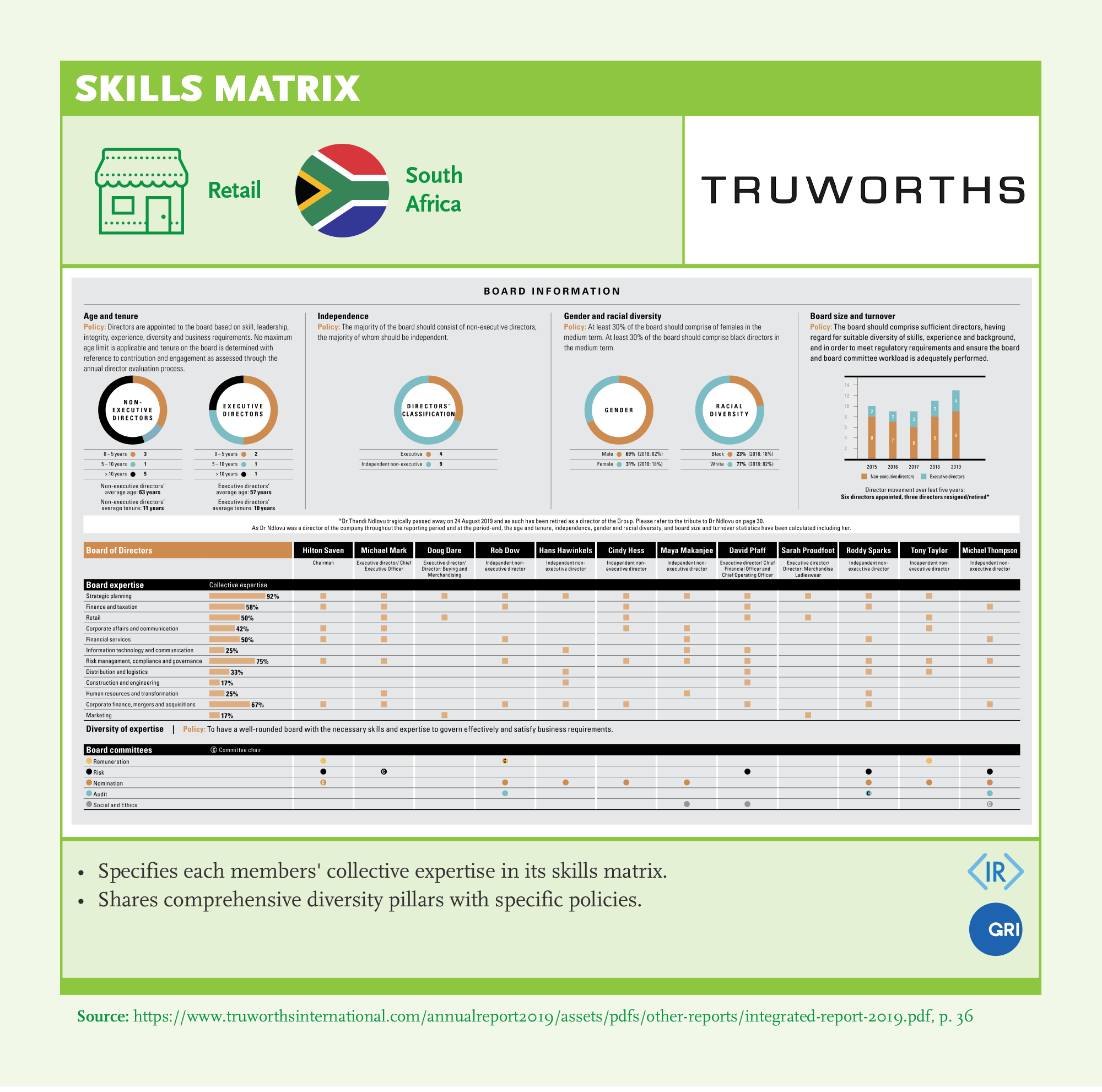

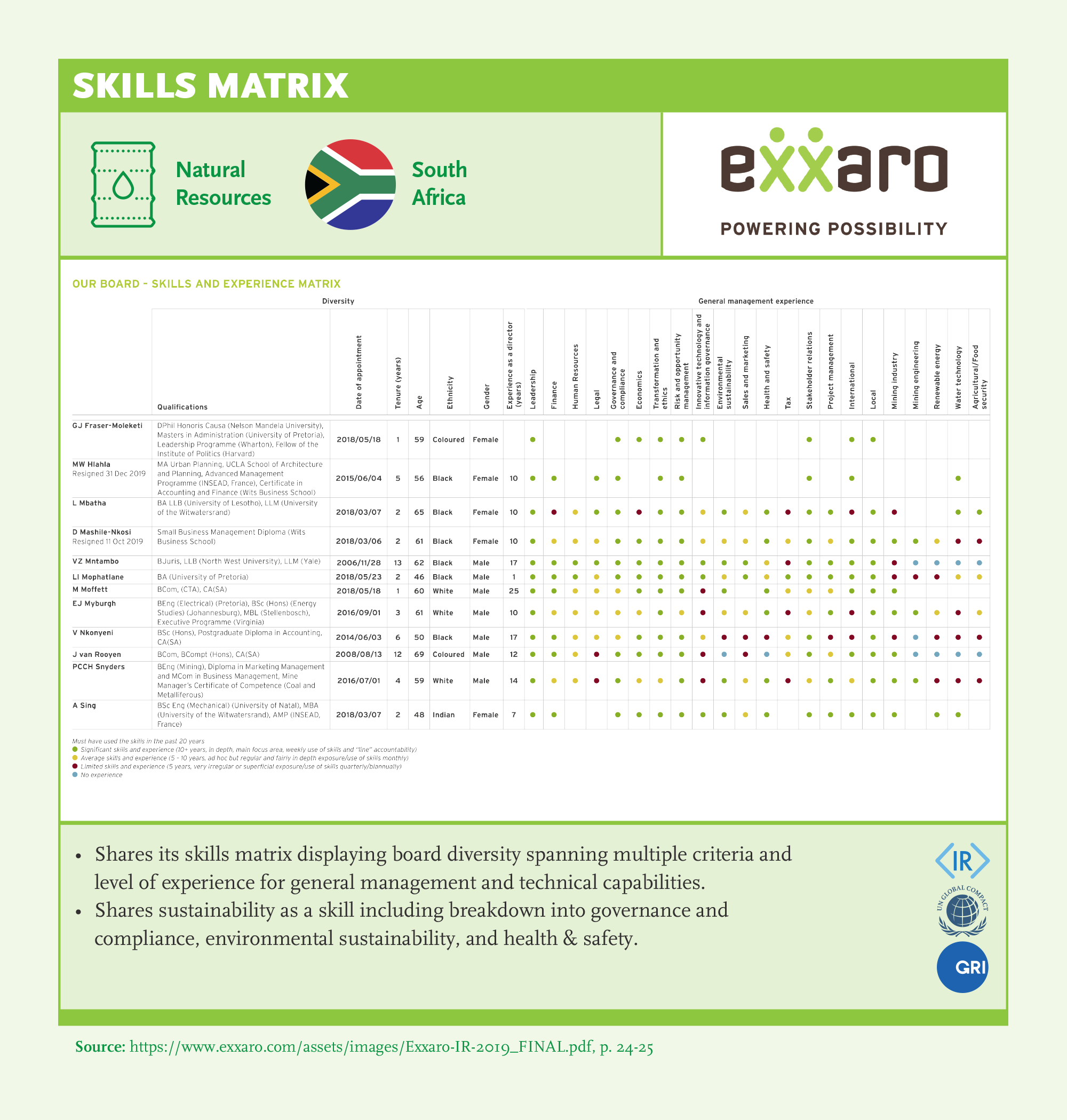

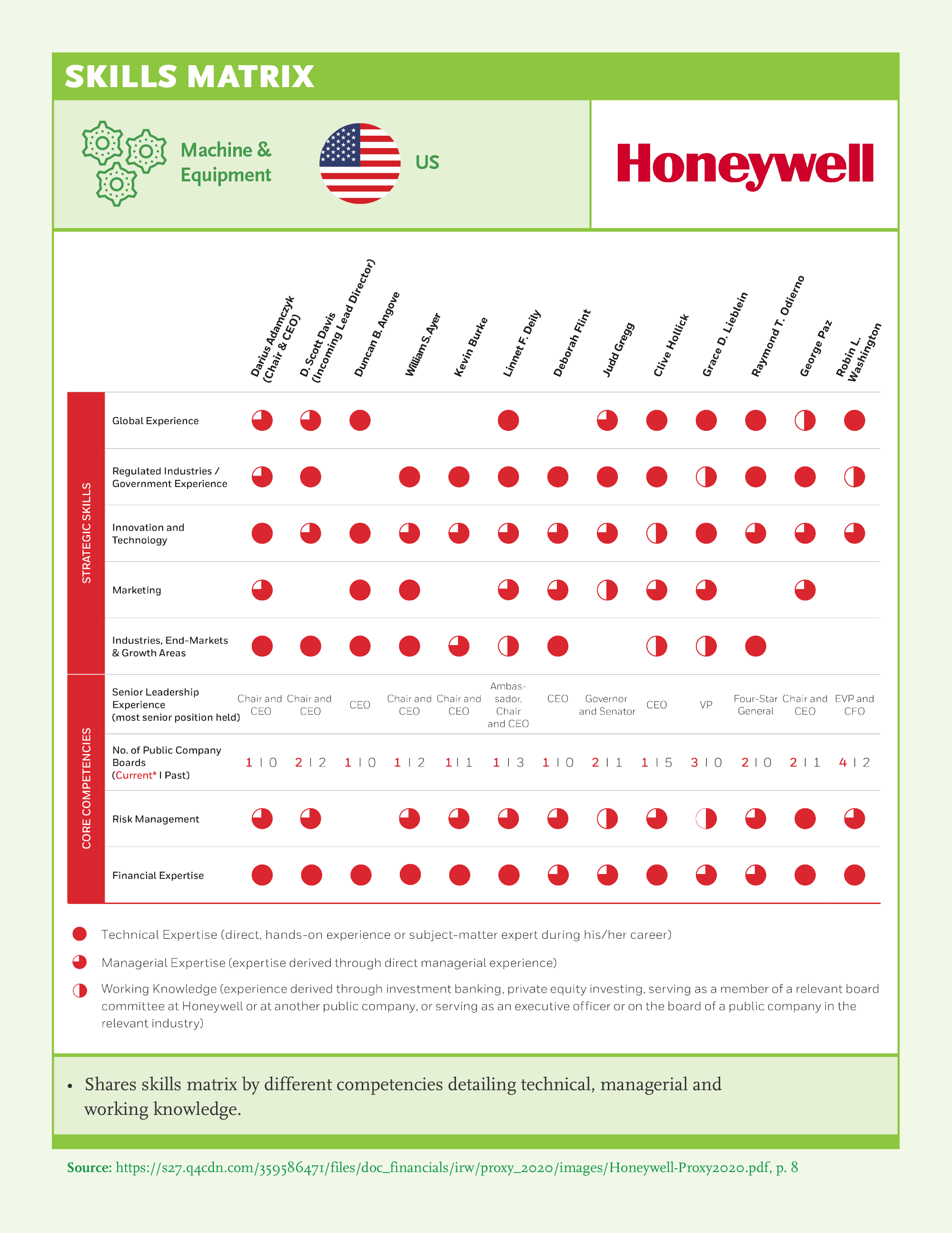

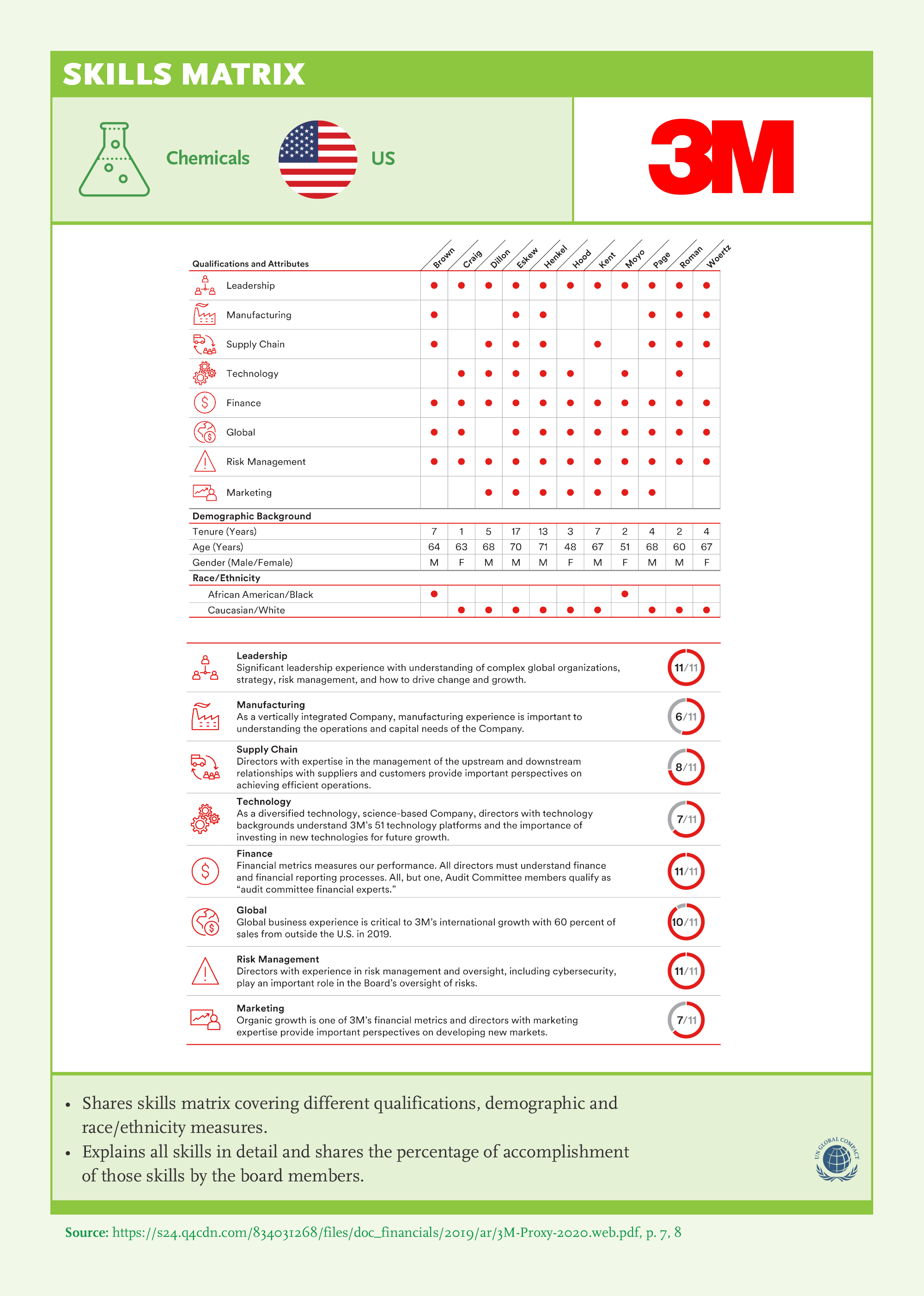

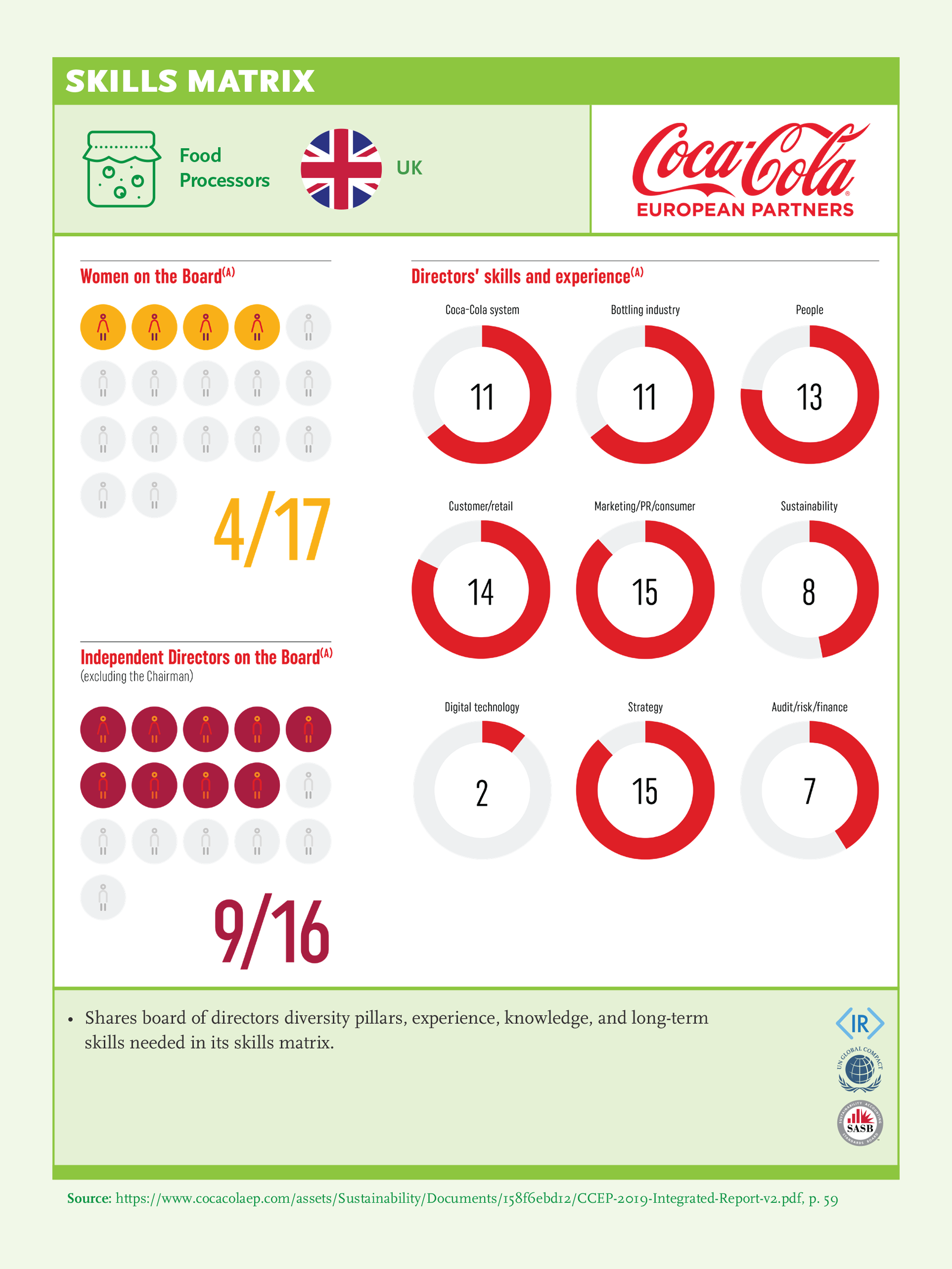

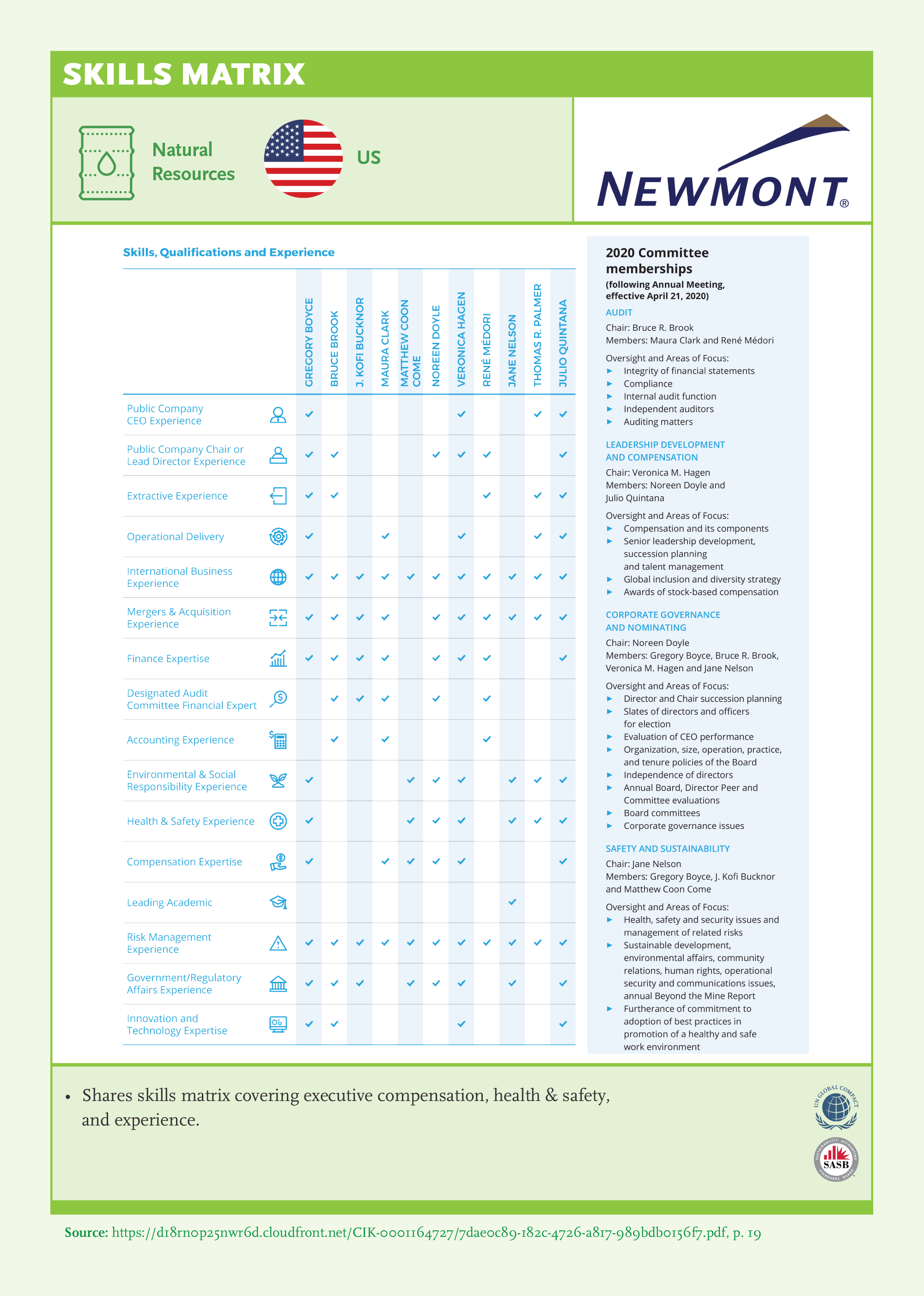

Skills Matrix

Board members need to have the right skills to provide guidance and oversight to the sustainability plans of the corporation. The Board needs to have sufficient expertise to understand the decision-making processes of key stakeholders, have members who are familiar with evolving sustainability standards and practices, and have sufficient diversity to adequately evaluate different dimensions, perspectives, and risks of sustainability issues.

A skills matrix identifies the skills, knowledge, experience, and capabilities desired from a board to enable it to meet both its current and future challenges and realize its opportunities. Disclosing a skills matrix is good governance and offers an opportunity to evaluate whether the board has the right skills and diversity to provide guidance and oversight on sustainability.

Recommendations

- 1Link business requirements to board qualifications and make sustainability a board priority.

- 2Publish a skills matrix.

- 3Focus on sustainability as a board skill.

- 4Increase diversity to manage sustainability.

- 5Foster productive dialogue among board members.

Key Findings

Our research reveals that the assessment of functional skills and the use of skill matrices is still not widespread. Comparing the past three years, boards’ leadership in sustainability increased in a significant amount, yet room for improvement still persists even among the leading companies.

- Percentage of companies that have at least one board member with sustainability as a skill, increased from 40% to 72%.

- Percentage of companies that disclose skills matrix increased from 36% to 54%, listing sustainability as a skill in skills matrix also increased from 8% to 34%.

- When we compare the past 3 years, there is a noticeable increase in disclosing the Skills Matrix. In 2019, only 21% of the companies had a skills matrix. This year, more than half of them (54%) have a skills matrix. It can be concluded that companies started paying attention to reviewing and publishing their skills matrix. A significant part of this increase is led by Indian companies with the release of a regulation by SEBI.

- More than 85% of Indian and US companies have at least one board member who has the ‘sustainability skill’, followed by South Africa, UK and Türkiye. In comparison to SGS 2020, there is an obvious improvement, regardless of geographic differences.

- In 2019, skills matrix sharing in India became enforced by regulations, which had a great impact. We assessed that 82% of Indian companies started to share their matrix in SGS 2021. This rate was 12% in SGS 2020. It shows that the rate of adoption increases when it is supported by governing bodies. The percentage of UK companies that share a skills matrix increased by 17% compared to the previous year, reaching 71%. None of the Turkish companies published a skills matrix, yet.

- While reviewing the skills matrix in depth, we analyzed whether sustainability is a listed skill. Especially in India, there has been an increase (+68%) in listing sustainability as a skill. Likewise, the percentage of South African companies listing sustainability as a skill increased by 33%.

- Pharmaceutical companies have a significant increase (more than 60%) in sharing sustainability as a skill in their skills matrices. 92% of pharma companies have at least one board member with sustainability as a skill. There is a 37% increase in the number of companies sharing their skills matrix in this industry.

- In the Automotive industry, the number of companies where sustainability skill is listed in their skills matrix reached 85% (58% increase compared to SGS 2020).

- Companies operating in Natural Resources are at the forefront in terms of the sustainability competence of boards in this year’s report, as it was last year as well.

- 48% of companies operating in Consumer Goods started to share a skills matrix this year, reaching 69% in total. However, progress is still needed as their skills matrix often does not include sustainability as a skill.

- GSLs that adopted initiatives or reporting standards are more likely to have at least one board member with sustainability as a skill in comparison to other companies.

- <IR> Reporting companies perform better in comparison to other initiatives. 81% of the Integrated Reporting companies have at least one board member with sustainability as a skill, 68% have a skills matrix, and 61% have listed sustainability as a skill. <IR> companies are followed by SASB, UNGC, and GRI companies in our SGS 2021 assessment.

Best Practice Examples

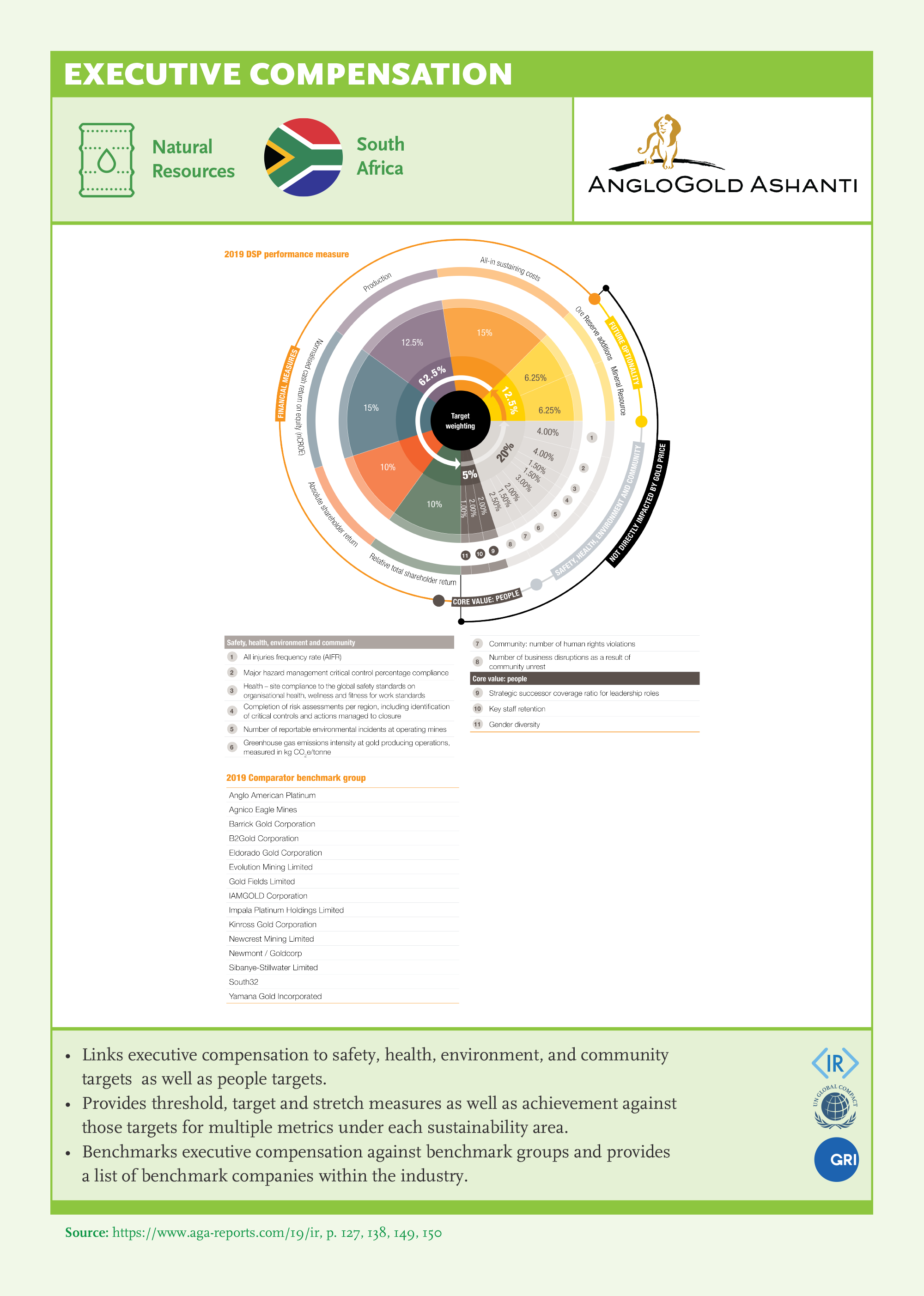

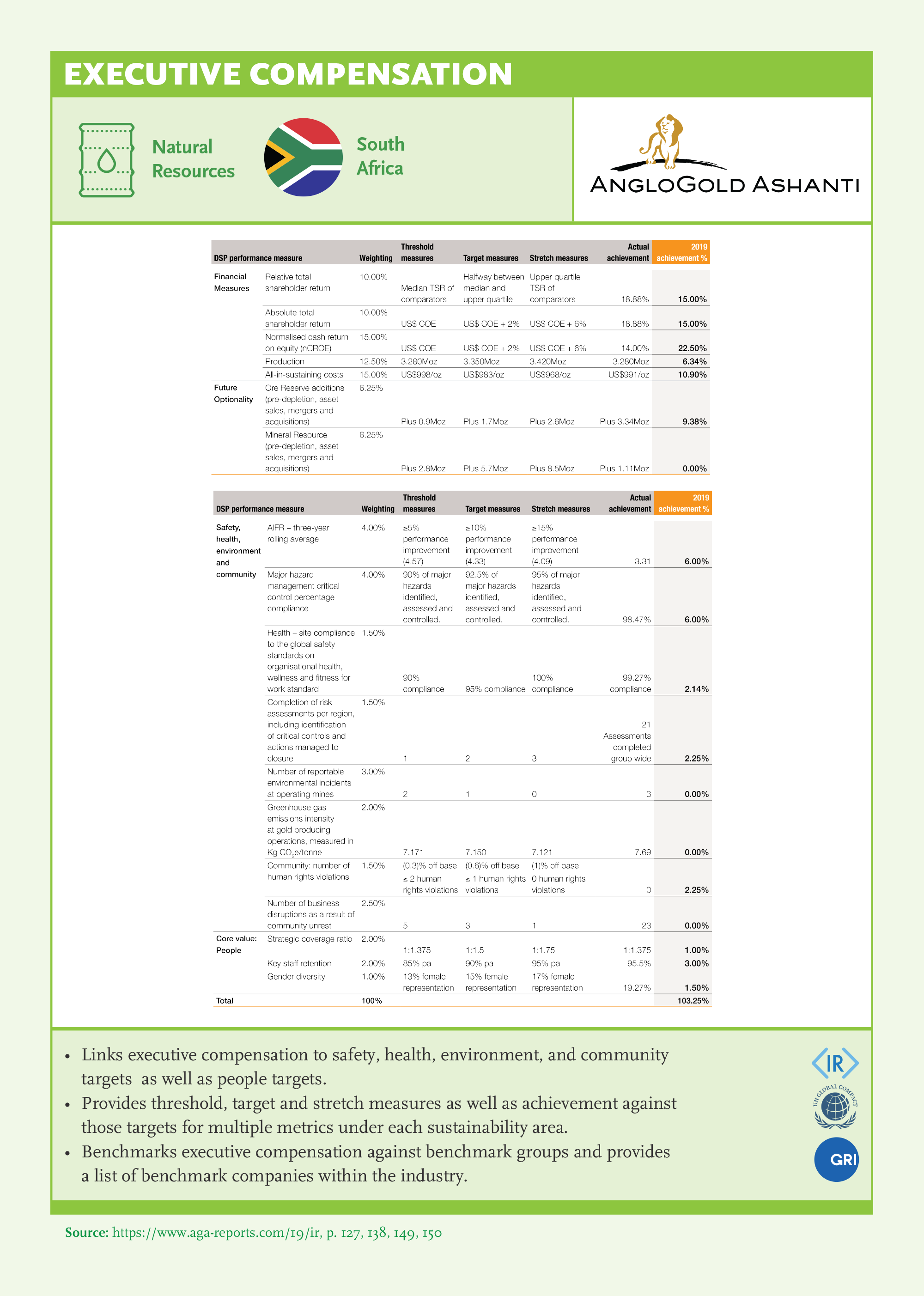

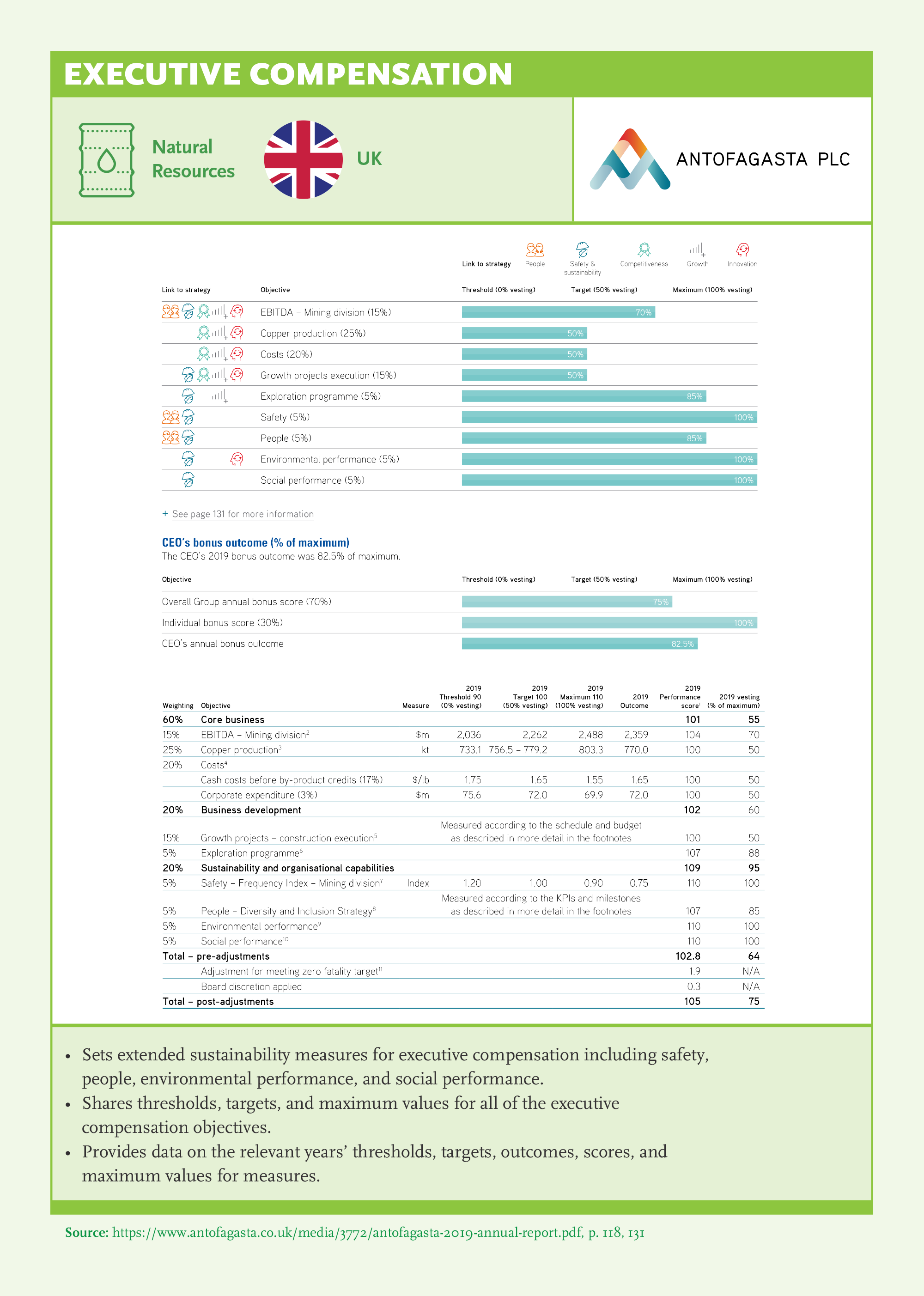

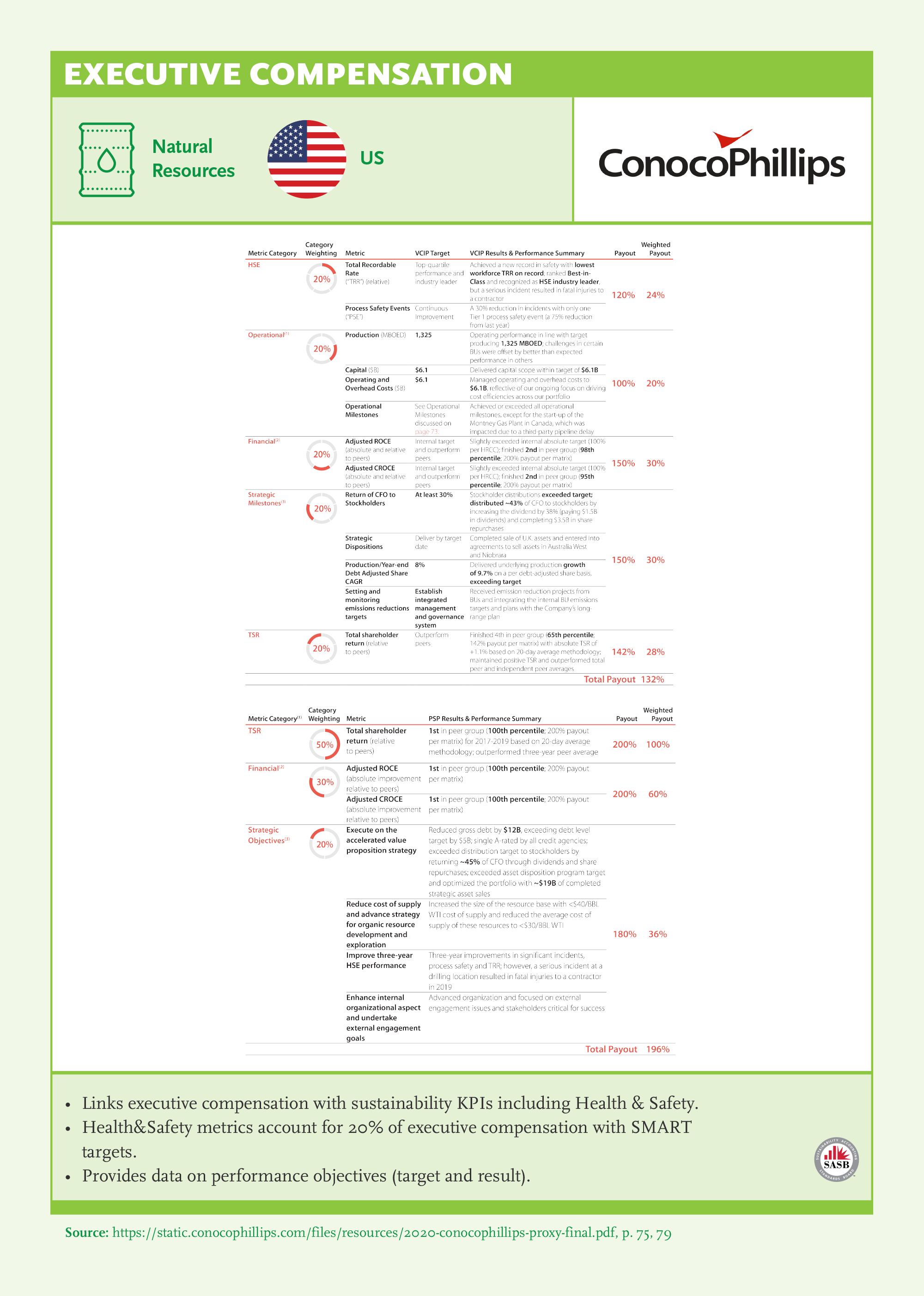

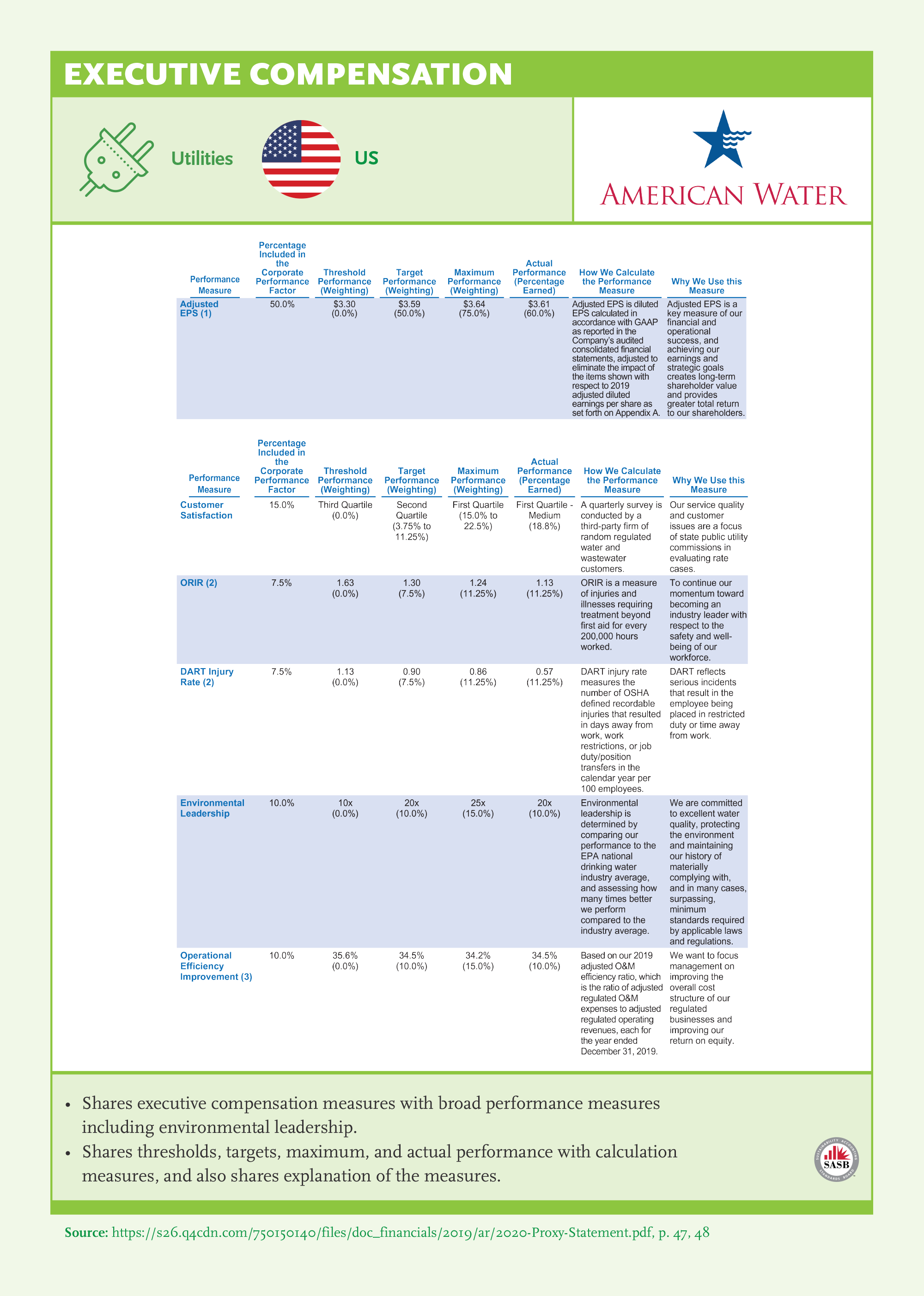

Executive Compensation

Boards need to make the management explicitly accountable for the company’s environmental and social impact and ensure that sustainability practices are adopted as everyday practice in decision making, to enhance the management’s ability to capture sustainability opportunities.

By aligning executive compensation with strategic sustainability targets and linking performance payouts to non-financial sustainability metrics, Boards can sharpen management’s focus on sustainability issues.

Recommendations

- 1Identify appropriate ESG metrics material to financial performance and align them with long-term strategy.

- 2Link executive compensation to material sustainability targets with a concentration on governance of all economic, environmental, and social issues.

- 3Provide high-quality disclosure to signal commitment to sustainability.

- 4Integrate sustainability into performance management systems of the entire organization.

Key Findings

- All companies share executive compensation. 88% share links to financial targets, but only 31% share links to sustainability targets.

- Percentage of companies that share executive compensation linked to sustainability KPIs reached 31% in SGS 2021.

- Companies focus more on social sustainability KPIs (28%), whereas only 18% link to environmental KPIs and 12% to governance KPIs.

- Leading countries in sharing sustainability KPIs are South Africa (62%), UK (44%), and US (35%). These countries were also leading in terms of sustainability KPIs in SGS 2020. However, Germany has the highest improvement in sharing sustainability KPIs, mostly in social issues (+19% compared to SGS 2020).

- Natural Resources companies are leading (63%) in sustainability KPIs sharing. Whereas the industry that is lagging is Retail (8%). Although 92% of retail companies share their KPIs, sharing sustainability KPIs is very low among them.

- Pharma companies have the highest improvement in sharing sustainability KPIs when compared with SGS 2020 (+19%). The sustainability KPIs are mostly related to social issues.

- GSLs that adopt at least one of the initiatives outperform in sharing sustainability KPIs in comparison to the companies which do not adopt any. More than 90% of SASB and <IR> companies set their sustainability KPIs.

Best Practice Examples

Guidance & Oversight

The Board is responsible for setting the company’s direction and sets the tone at the top. Right guidance is required for companies to manage risks and capitalize on opportunities related to sustainability, as well as taking a leadership role in creating a more sustainable future. Boards should ensure that sustainability issues are integrated into the company’s strategy and reflected in its policies and practices. Responsible Boards provide guidance to ensure the comprehensiveness of scope for sustainability by integrating governance of all economic, environmental, and social issues into the company’s value proposition, policies, and strategy.

The board’s oversight role requires setting up an effective internal control mechanism –ensuring the independence of audit and strict compliance, monitoring ethics and business conduct within the company and its value chain– and transparency in external reporting and disclosure. Effective tracking of sustainability performance and communication to the board is essential for improving oversight of sustainability.

Board structures for sustainability governance should be defined at the Board level and can include Direct Board Oversight or Sustainability Committee. Management responsibility should also be explicitly defined. To provide effective oversight, Boards should adopt an assurance framework that includes internal and external audit functions and timely reporting of key information to the Board to assess sustainability risks and opportunities.

Recommendations

- 1The Board should provide guidance on sustainability and set the tone at the top.

- 2Define commitments for sustainability through policy. Ensure that sustainability policies cover governance of all economic, environmental, and social dimensions.

- 3Ensure that policy covers and is adopted by all relevant stakeholder groups.

- 4Regularly review the policies.

- 5Define the Board’s sustainability responsibilities.

- 6Set up formal structures and ensure regular Board review of economic, environmental, and social issues, and governance of all.

- 7Cascade responsibility on sustainability across the organization.

- 8Focus on risks and opportunities.

- 9Ensure internal and independent audits cover all material G(EES) issues, supply chain, and geographies.

- 10Conduct board evaluation, integrate G(EES) issues into board evaluation and disclose results.

Key Findings

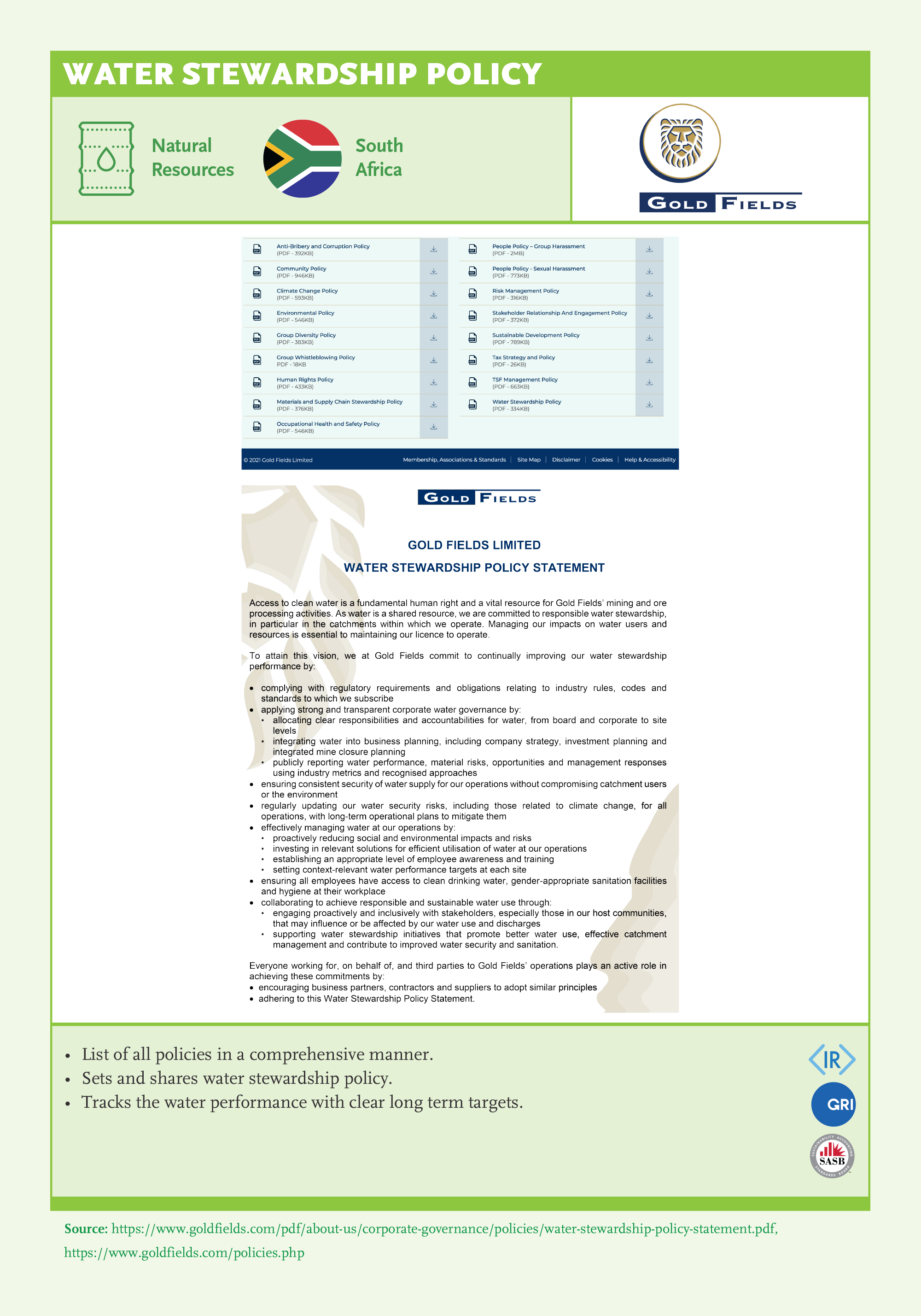

Setting Policies

Achieving sustainability goals require establishing sustainability policies and practices to guide company and employee behavior on a range of issues material to the company’s ability to create value. Policies can cover a wide range of matters and can differ between companies. A list of policies we looked for, and our findings are shown in the table below:

All GSLs set policies for E, S, G (100% for all).

- Environmental Policy: All the companies have an energy policy. More than 90% have climate change, waste & packaging, and water policy. The potential for improvement in developing policies on responsible sourcing, hazardous materials, and biodiversity remains as we highlighted in SGS 2020 (Biodiversity increased by 18%, Hazardous Materials by 17%, and Responsible Sourcing by 11%). All countries increased their performance of policy sharing in biodiversity.

- Social Policy: All the companies have occupational health and safety policies. More than 90% of GSLs cover diversity and inclusion, talent development and employee wellbeing, human rights, labor practices, data security and customer privacy, and product design & portfolio in their policies. There is room for improvement in social responsibility, local communities and labor rights policy and disclosure. In SGS 2021, it can be seen that setting policies in data security and customer privacy gained importance among the GSLs (9% increase). South African, US, and German companies increased their policy sharing ratio in data security and customer privacy more than 10% which leads all the companies in those countries to set relevant policies.

- Governance Policy: Governance policies of GSLs cover compliance related issues, risk management, executive compensation, supplier code of conduct, related party transactions, and board diversity. Succession planning and donations policies have the lowest ratio. Disclosing Board Diversity (+18%), Succession Planning (+17%), and Related Party Transaction (+13%) policies increased in comparison to the previous year. The highest increase in succession planning is in Germany, India, and Türkiye (in which bases were lower). The policies related to Donations remain with the highest improvement potential as it was in SGS 2020.

Board’s Oversight Responsibilities

The Board is responsible for providing oversight on sustainability issues, reviewing and deciding on the risk appetite and monitoring implementation throughout the organization. The board’s oversight role requires setting up an effective internal control mechanism, ensuring the independence of audit and strict compliance, monitoring ethics and business conduct within the company and its value chain, and transparency in external reporting and disclosure. Effective tracking of sustainability performance and communication to the board is essential for improving oversight of sustainability.

- The most improved area in oversight is related to the Customer Community in comparison to SGS 2020 (+18%, SGS 2021: 89%).

- Customer Community-related areas are followed by the Board’s leadership in setting materiality thresholds; however, there is still potential for development (+12%, SGS 2021: 62%).

- Another area for improvement is the donations policy. Setting policies and providing oversight to donations should be under the Board’s responsibility (+13%; SGS 2021: 66%). Even if there is an increase in this area, the development potential remains, especially in Germany and the US.

- Access to Information/Independent Advice is listed frequently in Charters, however it still has the highest potential for improvement (SGS 2021: 81%).

Independent Audit and Access to Information

Independent audits of sustainability performance and processes are important for transparency purposes. However, the external assurance for sustainability issues is still very low. It may be because sustainability has diverse topics, quantitative as well as qualitative metrics which are difficult to measure. Furthermore, the material sustainability issues vary by industries and even by companies in the same industry. Consistent external assurance and disclosure for sustainability issues can enable the development of standards in sustainability reporting and provide investors with increased confidence in the quality of sustainability performance data, thereby making it useful for decision-making.

- GSLs increase their percentage in internal audit sustainability coverage by broadening the subtopics of E, S, G (+14%, +12%, +4% respectively). In terms of countries, Germany and Türkiye increased the coverage of social issues in independent audits (+25%). All companies report directly to the Board in internal audits.

- Independent audit coverage of sustainability increased at the same rate as independent audit. Independent audits in governance related topics increased by 11% and closed the gap with environmental and social issues.

- In addition, the supply chain coverage in independent auditing improved in comparison to SGS 2020 (+12%, SGS 2021: 59%).